Fresh Issue vs OFS: Key Differences Every IPO Investor Should Know

- Fresh Issue vs OFS — Core Definitions and Mechanics

- Historical IPO Examples — How the Structure Has Played Out

- What OFS Structure Signals About Seller Intent?

- How to Read a DRHP for Fresh Issue vs OFS Information?

- Fresh Issue vs OFS: Which Is Better for Investors?

- Conclusion

- Frequently Asked Questions

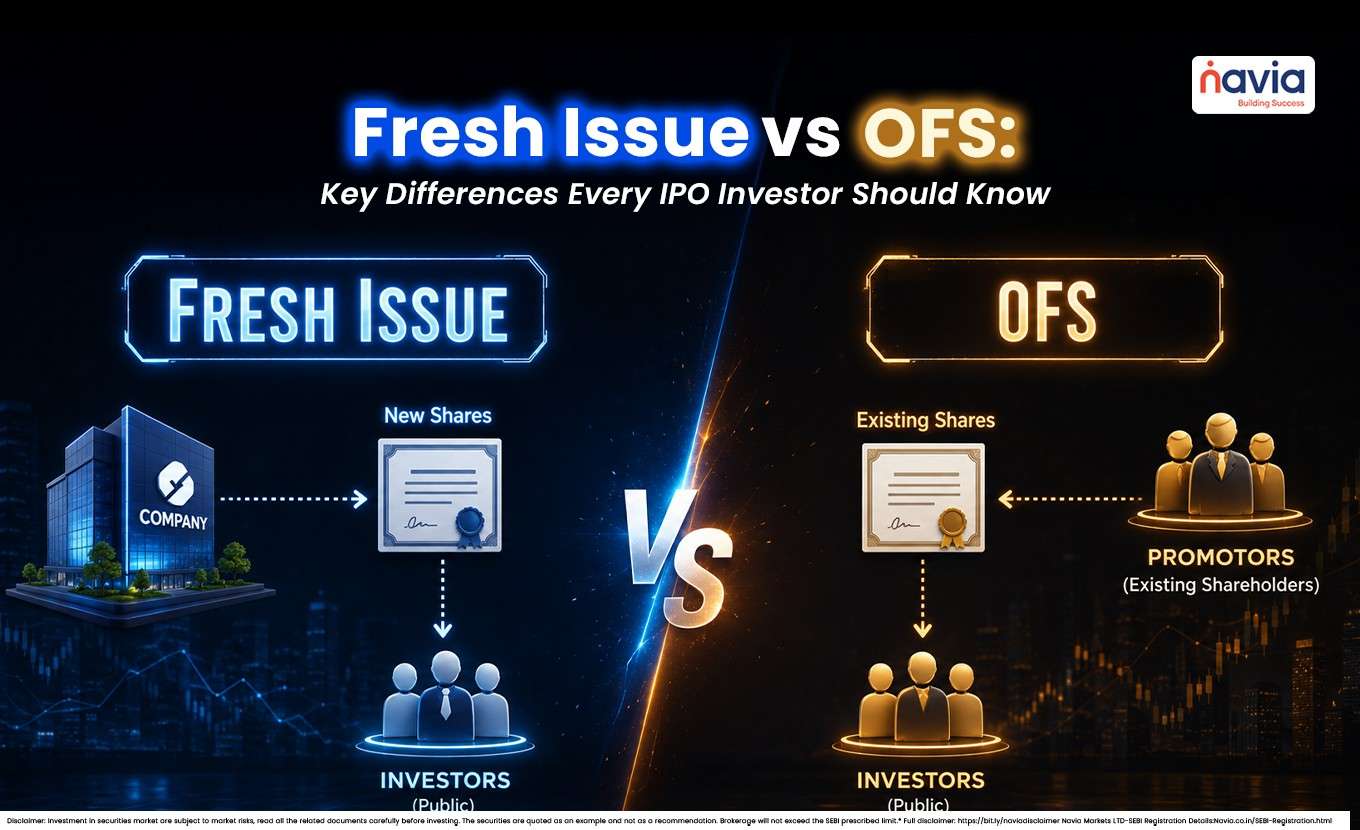

When you apply for an IPO, one of the first things to check is whether it is a fresh issue vs OFS offer or a mix of both. This matters because it tells you where the money is going and whether the company is raising new capital or existing shareholders are selling their stake.

In simple terms, the difference between fresh issue and offer for sale is about who receives the proceeds and what happens to the company’s share capital. Understanding this helps investors read IPO documents better and make more informed decisions.

Fresh Issue vs OFS — Core Definitions and Mechanics

A fresh issue creates new shares that did not exist before. The company collects the subscription money and uses it for business purposes. An OFS takes existing shares — already held by promoters, PE funds, or institutional investors — and sells them to the public. No new shares. No new capital for the company.

Side-by-Side Comparison with the NSE IPO as Live Reference

| Feature | Fresh Issue | Offer for Sale (OFS) | NSE IPO 2026 (Real Example) |

|---|---|---|---|

| Shares created? | YES — new shares issued | NO — existing shares change hands | NO — 100% OFS. DRHP states: Fresh Issue: Not applicable |

| Who gets the money? | The COMPANY receives all proceeds | Selling SHAREHOLDERS receive proceeds | SBI, CPPIB, Morgan Stanley, and other sellers — not NSE |

| Effect on share capital | Increases outstanding shares | No change in total share count | NSE’s share count stays at 247.5 crore shares |

| Equity dilution? | YES — existing holders get diluted | NO — dilution already happened earlier | None — 6.02% of existing shares just change owner |

| Company capital benefit? | YES — company can invest proceeds | NO — no fresh capital for business | NSE raises zero rupees. It is already highly profitable |

| Promoter stake effect | Existing holders Diluted proportionally | Promoter/investor reduces stake | LIC (largest shareholder, 10.72%) is not participating in the OFS. Investors may consider this along with other publicly available information when evaluating the IPO |

| Typical use case | Early-stage growth, debt repayment, capex | Promoter/PE exit, liquidity event, stake reduction | NSE shareholders cashing in — SBI’s cost was Rs.0.80/share vs expected IPO price of Rs.1,400+ |

Historical IPO Examples — How the Structure Has Played Out

Understanding fresh issue vs OFS in theory is useful. Seeing how it played out in major Indian IPOs makes it concrete.

| IPO | Year | Structure | Proceeds Went To | Outcome / Investor Takeaway |

|---|---|---|---|---|

| Zomato | 2021 | Fresh Issue: Rs.9,000cr + OFS: Rs.375cr | Company (fresh) + early investors (OFS) | Fresh issue funded expansion. OFS was small — promoters retained a significant shareholding after the IPO. Stock volatile but business grew. |

| Paytm (One97) | 2021 | 100% Fresh Issue | Company — Rs.18,300cr raised | Proceeds for growth but high cash burn raised questions. Stock fell sharply post-listing — fresh issue alone does not guarantee value. |

| LIC IPO | 2022 | 100% OFS — Government sold 3.5% stake | Government of India — no capital to LIC | Pure exit play. LIC needed no capital. Valuation and dividend yield were the key investment metrics — not use of proceeds. |

| Hyundai Motor India | 2024 | 100% OFS — Rs.27,859cr | Parent company Hyundai Korea — India entity received nothing | India’s then-largest IPO was pure OFS. Proceeds left India. Investors assessed solely on India business fundamentals and valuation. |

| NSE IPO 2026 | 2026 (pending) | 100% OFS — R s.25,000 30,000 cr est. | SBI, CPPIB, Morgan Stanley, and other sellers | NSE receives zero. Investors must assess exchange business on fundamentals: 93% market share, Rs.10,000cr+ profit, F&O; dependency risk, SEBI regulatory overhang. |

What OFS Structure Signals About Seller Intent?

An OFS is not inherently positive or negative. The same structure — existing shareholders selling — can mean very different things depending on WHO is selling, HOW MUCH they are selling, and WHAT THEY ARE KEEPING.

The NSE IPO Seller Landscape

🔵 SBI (largest seller): 2.48 crore shares. Cost: Rs.0.80/share. Selling after decades. SBI’s sale may be viewed as a portfolio monetization event. Investors should avoid drawing conclusions based solely on the sale.

🔵 CPPIB (Canada Pension Plan): Long-term institutional holder. Partial exit — not selling entire stake.

🔵 Morgan Stanley and other global institutions: Part of the original institutional investor base from before NSE went electronically.

🔵 LIC (NOT selling): LIC is the largest shareholder at 10.72% and has chosen NOT to participate. Investors may consider both participating and non-participating shareholders as one of several factors while evaluating the IPO.

How to Read a DRHP for Fresh Issue vs OFS Information?

Every piece of information you need is in the DRHP. The challenge is knowing where to look. The checklist below maps each key question to its exact location in a standard Indian IPO prospectus.

| What to Check in DRHP | Where to Find It | Fresh Issue Flag | OFS Flag | NSE IPO 2026 Example |

|---|---|---|---|---|

| Issue structure breakdown | Cover page and Objects section | ‘Fresh Issue of X shares’ | ‘Offer for Sale of Y shares by Selling Shareholders’ | DRHP states: Offer for Sale of up to 14,89,05,525 equity shares. Fresh Issue: Not applicable. |

| Use of proceeds | Objects of the Issue chapter | Specific line items: capex Rs.X, debt repayment Rs.Y, working capital Rs.Z | ‘The company will not receive any proceeds from the OFS’ | NSE DRHP: ‘The Company will not receive any proceeds from the Offer’ |

| Selling shareholder list | Offer for Sale section | Not applicable | Names, share quantities, and purpose of each seller | SBI: 2.48cr shares. CPPIB, MS Strategic, Aranda Investments, Bank of Baroda, etc. |

| Post-issue promoter holding | Shareholding pattern chapter | Check if promoter is above SEBI minimum post-IPO threshold | No change — OFS does not Affect promoter Holding directly | NSE has no promoter. LIC (10.72%) not selling. Holding structure unusual. |

| EPS impact calculation | Financial statements + issue details | Calculate post-issue diluted EPS — will be lower | No EPS change — no new shares | NSE FY26 EPS Rs.41.62 — unchanged post-IPO since it is 100% OFS |

| Appraiser for objects | Objects of the Issue | Required if proceeds include debt repayment above 25% of issue | Not applicable for OFS | Not applicable for NSE |

Fresh Issue vs OFS: Which Is Better for Investors?

There is no universal answer. The right structure depends on the company, the valuation, and what drives the investment case.

When Fresh Issue is More Relevant to Your Analysis

🔹Growth companies: A fresh issue funding expansion, R&D;, or market entry can accelerate the business — making the use of proceeds a key underwriting question.

🔹Debt reduction: If proceeds retire high-cost debt, the interest savings directly improve profitability — a quantifiable benefit from the fresh issue.

🔹Capex deployment: Specific capital projects (new plants, technology infrastructure, fleet expansion) with clear return on investment timelines may help investors evaluate whether the dilution aligns with the company’s stated growth plans.

🔹Valuation discipline: Calculate post-issue EPS before comparing P/E ratios — a fresh issue can make the stock look cheaper on pre-issue EPS than it is.

When OFS Structure Shifts Your Analysis

🔹 Business quality becomes the entire thesis: No fresh capital = no new growth levers from IPO proceeds. The business must stand on its existing merits.

🔹 Seller motivation matters more: Understand WHY they are selling now. Is it regulatory requirement (minimum public holding)? PE fund lifecycle? Personal estate planning?

🔹 Valuation peer comparison is sharper: Without proceeds-based growth, valuation must be compared against sector peers on existing metrics — P/E, EV/EBITDA, dividend yield.

🔹 Non-selling shareholders are a signal: LIC not selling in the NSE IPO is as informative as who IS selling. The decision not to participate in an OFS reflects conviction about future value.

Conclusion

The difference between fresh issue and offer for sale is straightforward once you know who is issuing the shares and where the money goes. A fresh issue brings new capital into the company, while OFS transfers ownership without adding fresh capital to the business.

So, when you compare fresh issue vs ofs, do not look at the label alone. Check the valuation, business strength, and use of proceeds, because those factors are also important considerations alongside the IPO structure than the structure by itself.

Do You Find This Interesting?

We’d Love to Hear from you-

Frequently Asked Questions

What is a fresh issue in an IPO?

A fresh issue is when a company creates and sells new shares to the public. The money raised goes directly to the company and is used for purposes stated in the DRHP — such as expansion, debt repayment, or working capital. Fresh issues dilute existing shareholders.

What is an Offer for Sale (OFS)?

An OFS is when existing shareholders (promoters, PE investors, institutions) sell their shares to the public. No new shares are created. The company receives no money — proceeds go entirely to the selling shareholders.

How does fresh issue affect EPS?

Fresh issue increases the total share count. If the company’s profit does not grow proportionally, EPS falls. Example: A fresh issue of 25% more shares dilutes EPS by 20% immediately. OFS does not affect EPS because no new shares are created.

What should I check if an IPO is mostly OFS?

Focus entirely on valuation (P/E, P/B), business quality, growth trajectory, and seller motivation. Since no fresh capital enters the company, the investment case must stand on the company’s existing financial strength — not on how it plans to use IPO proceeds.

DISCLAIMER: Investment in securities market are subject to market risks, read all the related documents carefully before investing. The securities quoted are exemplary and are not recommendatory. Full disclaimer: https://bit.ly/naviadisclaimer.