The UPI Illusion: Why Your Brain Thinks You’re Not Really Spending!

Moving money in India used to be a real test of patience! Transferring money felt like hunting for bank details and struggling with slow confusing banking websites. Paying a small street vendor usually involved searching for change, or even worse, an unspoken apology when you hand over a ₹2000 note for a ₹25 chai. The whole process wasn’t just complicated; it simply did not align with our fast-moving life.

Gradually, payment methods started to evolve for the better with the increasing adoption of digital payments—transactions carried out via electronic platforms like mobile applications, cards, or online banking. Slowly transferring funds became easier, reducing the need for physical cash. However, even with the greater availability of these tools, many payment experiences continued to be inconvenient and not secure.

What is UPI?

To simplify everyday payment challenges, ‘Unified Payment Interface’ (UPI) was launched on April 11, 2016, by National Payments Corporation of India (NPCI). This innovation was designed to allow users to link multiple bank accounts into a single mobile application. Consequently, banks throughout India developed their own UPI-enabled app for Android, iOS, and Windows platforms. The use of UPI reshaped the digital payment landscape by unifying services like fund routing and merchant payments and peer-to-peer (P2P) payment transfers, making the payment process convenient and user-friendly.

Currently, UPI processes an impressive 18.67 billion transactions monthly, equating more than 600 million transactions daily. That amounts to almost 7,000 transactions each second, reflecting the massive scale and adoption of UPI in Indian’s digital payment ecosystem. According to NPCI data (Sept 2024), UPI volumes have grown exponentially — processing billions of transactions annually.

Source: NPCI, Ministry of Finance (20 SEP 2024) by PIB Delhi

| Year | Transaction Volume (in crore) | Transaction Value (in lakh crore) | Volume YoY Growth % | Value YoY Growth % |

| 2017-2018 | 92 | 1 | – | – |

| 2018-2019 | 535 | 9 | 481.52% | 800.00% |

| 2019-2020 | 1,252 | 21 | 133.80% | 133.33% |

| 2020-2021 | 2,233 | 41 | 78.37% | 95.24% |

| 2021-2022 | 4,597 | 84 | 105.84% | 104.88% |

| 2022-2023 | 8,375 | 139 | 82.20% | 65.48% |

| 2023-2024 | 13,116 | 200 | 56.56% | 43.88% |

Cash Vs UPI, What’s the Difference?

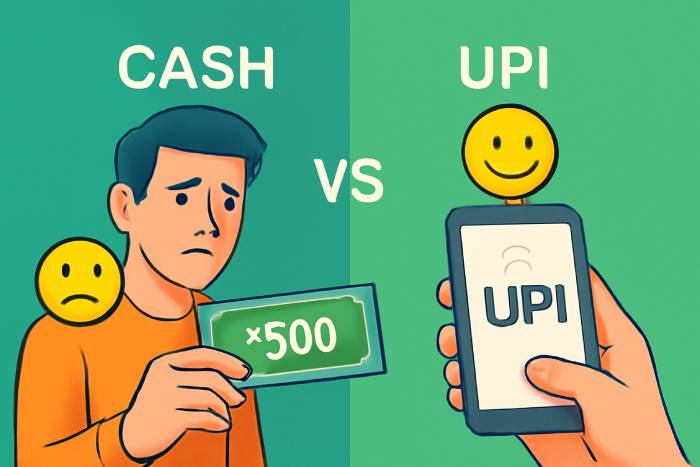

Remember when handing over the five crisp ₹100 notes was the only way to pay ₹500? You would open the wallet, double-check if the amount was right, hesitate for a second, and perhaps even ask yourself, “Do I really need this?”. That little pause gave your brain a moment to process the expense—making the process feel more real.

Now? It’s all done in a tap and a beep. No pause, no wait, no second thought. That’s UPI in action! With UPI, your money slips away so quietly. Psychologically, it’s a completely different experience. ₹500 paid via UPI doesn’t hurt the way it does in cash because your brain barely registers the loss. What once was a conscious choice is now an unconscious habit—and that’s the illusion.

While cash and digital payments, UPI in particular both facilitate the same purpose of transferring money; they create fundamentally different psychological experiences. Here is how cash and UPI differ in a way they influence our spending behavior and psychology.

| Aspect | Cash | UPI |

| Pain of Paying Activation | High | Low |

| Memory Encoding | People remember their spending vividly | Tend to be easily forgotten |

| Impulse Control Delay | Adds hesitation and pause | Skips reconsideration |

| Dopamine Activation | Limited gratification | Instant gratification |

| Spending Feedback Loop | Immediate feedback–cash depletes visually | Delayed or hidden feedback–-balance checked less often |

The Surprising “Pleasure of Paying” and Reward Systems!

Interestingly, some studies even suggest that mobile payments don’t just reduce the ‘pain of paying’ but can also trigger a ‘pleasure of paying’. Why? Because the process is so instant and effortless, it activates the brain’s reward system— particularly the nucleus accumbens, which are linked to feelings of satisfaction and gratification.

That little dopamine hit you get from a fast successful payment reinforces the habit of spending. Over time, the brain starts associating spending with pleasure and is more likely to spend it impulsively and frequently. As a result, your brain finds it difficult to associate spending with actual financial outflow. But there is more than just the absence of pain.

The Psychology of Effortless Payments

When paying becomes too easy, thinking before spending becomes optional. This is exactly where the problem begins as this frictionless flow rewires our relationship with money. 2016 research published in the Journal of Consumer Psychology reveals that these kinds of payments weaken self-regulation, increasing the likelihood of micro spending, impulse purchases, and budget overruns.

The more effortless it feels, the less aware you become of what you are actually giving up. In an IIT Delhi study of 276 users found that 74% of them reported that they were spending more after adopting UPI and 60% confessed it was because they did not ‘feel’ the money departing from their accounts. Because the money isn’t seen or felt, your brain skips the usual ‘pain of paying’ response, making it easier to overspend. Digital payments reduce friction, which can make spending feel less noticeable and may affect financial awareness.

Spend with Awareness, Not Regret!

It’s not about reducing expenses—it’s about being more strategic with your spending. In a world where payments happen in seconds, your edge comes from how well you stay mindful. Here’s how to build intentional habits using simple digital tools and strategies, so every payment supports your goals—not regrets.

Smart Spending Starts Here:

🠖 Identify Financial Goals: Understand whether your goal is to purchase a new gadget, save for vacation or different issues, so you have solid motivation to resist your impulsive spending habits. Every time you resist something you simply want– but don’t truly need–you take a step closer to your financial goal.

🠖 Set Clear Financial Goals: Instead of “save more”, go specific– “Save ₹X for a down payment by Y date”. When spending, ask yourself whether the purchase is moving you closer or further from that goal. You now have a compelling reason to be mindful of your financial behavior.

🠖 Put saving as a priority ahead of spending: Before you spend, Move a portion of your income into a separate dedicated savings account (with separate UPI ID if possible). This isolates your financial opportunity to meet your goals before making a purchase.

🠖 Pause before you pay: Before confirming any UPI transaction, take a mindful breath and ask yourself if it aligns with your financial objectives. A few seconds of reflection can help prevent unnecessary spending.

🠖 Review your transaction history: Most UPI apps include transaction logs for easy review. Get into the habit of reviewing them on a daily or weekly basis. You’ll recognize spending patterns, spot impulsive purchases, and get better control of your spending habits.

Conclusion

UPI has revolutionized the way we spend—fast, easy, and secure. But ease shouldn’t mean mindless spending. The answer is not deleting the app or feeling guilty—instead, bringing back intention. With every tap lies a choice—and the more mindful you are, the stronger that choice becomes. Therefore, spend with purpose, not impulse—and let your money work for you, not against you.

For more insights on money and investing behavior, explore resources from Navia Markets.

Do You Find This Interesting?

We’d Love to Hear from you-

Frequently Asked Questions

Can UPI replace cash entirely?

While UPI is more user-friendly and convenient. Cash still plays a role in places where there is low access to digital platforms.

Does UPI have transaction charges?

Most of the transaction costs are free while some banks charge for high-value or frequent transactions.

Is it possible to cancel the UPI transaction?

No, the transaction cannot be cancelled or reversed once it is processed. We should double-check before we confirm it.

Will UPI work without Internet access?

Yes, UPI can work offline using USSD codes, but features may be limited comparatively.

Does UPI provide security?

UPI ensures security by using encryption and two-factor authentication. It’s highly secure when it’s used responsibly.

DISCLAIMER: Investments in securities market are subject to market risks, read all the related documents carefully before investing. The securities quoted are exemplary and are not recommendatory. Full disclaimer: https://bit.ly/naviadisclaimer.