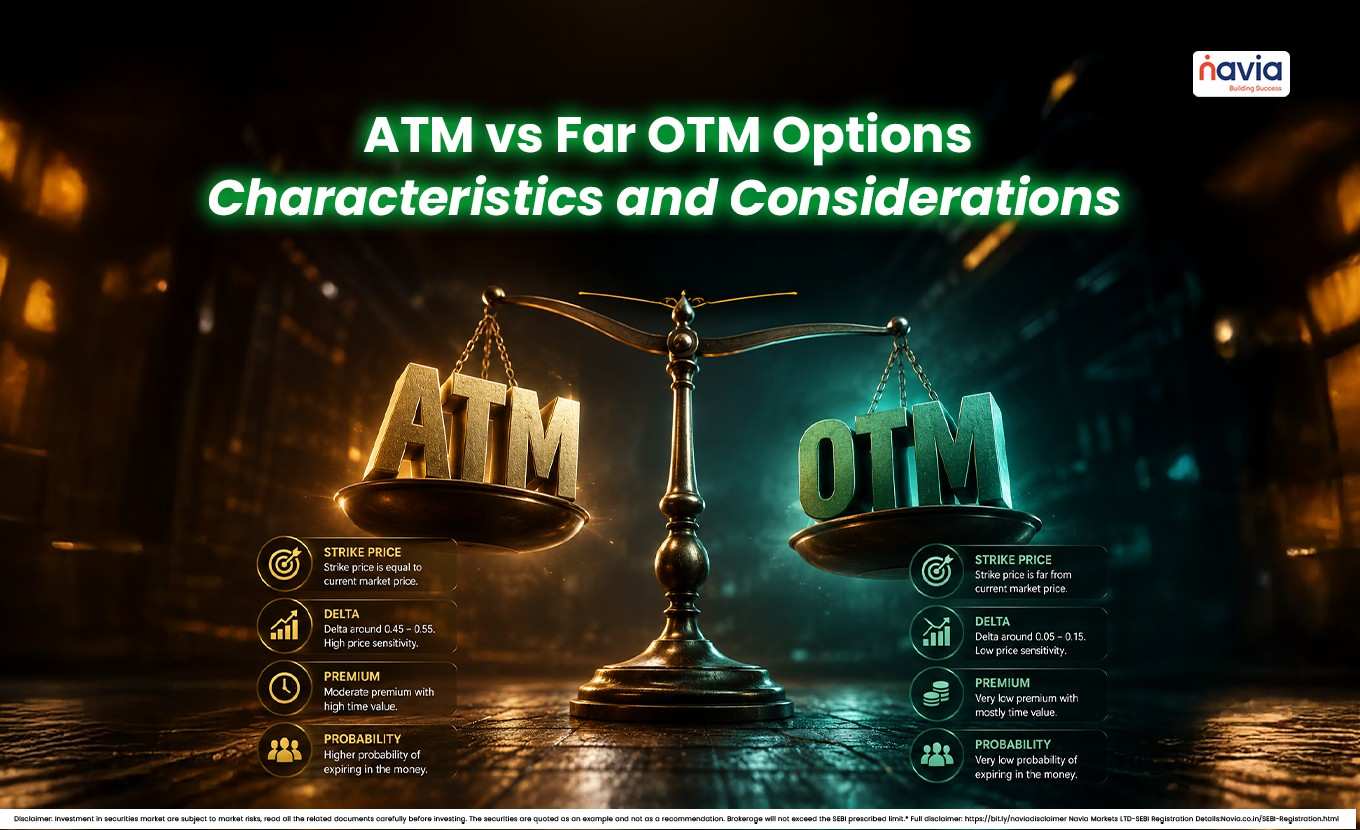

ATM vs Far OTM Options: Characteristics and Considerations

- What is At The Money?

- What is Out of The Money?

- How ATM and Far OTM Options Behave Differently?

- Payoff Scenarios: Rupee-by-Rupee Comparison

- Intrinsic Value vs. Time Value — The Component Breakdown

- When to Use Which Strike — Scenario-Based Guide

- Conclusion

- Frequently Asked Questions

When traders compare option strikes, the real question is not how many contracts they can buy, but how much value those contracts may carry. That is why the debate around at the money and far out of the money strikes matters so much in options trading.

In simple terms, ATM vs Far OTM Options is a discussion about balance versus cheapness. An at the money option usually has a better blend of responsiveness and tradability, while far OTM options may look cheaper but often need a much bigger move to become useful.

What is At The Money?

A what is at the money option question is easy to answer: it is an option whose strike price is equal to, or very close to, the current market price of the underlying asset. The at the money option meaning is therefore tied to the current spot price rather than a future guess.

Because the option is already near the market price, its value tends to react more sharply to movement in the underlying asset. That is why many traders prefer ATM strikes when they want a more direct connection to price action.

What is Out of The Money?

To understand what is out of the money, think of an option whose strike is not yet favorable compared with the current market price. The out of the money means the option currently has no intrinsic value and would not be profitable if exercised immediately.

So, what is out of the money option in practical terms? For calls, the strike is above the current market price; for puts, the strike is below it. These options may still gain value if the market moves strongly enough, but they usually need a much larger move than ATM options.

How ATM and Far OTM Options Behave Differently?

The Option Greeks quantify the sensitivities of an option’s price to various factors. Understanding how Greeks differ between ATM and far OTM is the most important technical insight for strike selection.

| Greek / Metric | ATM Option | Far OTM Option | What It Means in Practice |

|---|---|---|---|

| Delta | ~0.50 | ~0.10 – 0.20 | ATM reacts to every rupee move; OTM largely ignores small moves |

| Gamma | Highest | Low | ATM delta changes fastest — amplifies gains and losses |

| Theta (Time Decay) | Moderate | Fastest (% of premium) | OTM loses time value disproportionately fast near expiry |

| Vega (Vol Sensitivity) | High | Low | ATM gains most from a volatility spike (e.g. pre-event) |

| Probability of Profit | ~45-50% | ~5-15% | ATM is near fair-coin odds; far OTM is a long shot |

| Intrinsic Value | Near zero | Zero | Neither has intrinsic value; both are purely time + vol premium |

Delta Deep Dive

Delta = Change in Option Price / Change in Underlying Price

An ATM option with delta ~0.50 means: for every Rs. 1 move in Nifty, the option moves ~Rs. 0.50. A far OTM option with delta ~0.10 means it moves only Rs. 0.10 for the same Rs. 1 move. You need 5x the underlying movement to generate the same nominal gain from a far OTM contract.

Gamma — The Acceleration Factor

Gamma = Change in Delta / Change in Underlying Price

ATM options have the highest gamma. This means their delta changes most rapidly with price movement — a double-edged sword. A large move in your favour causes delta to increase, amplifying gains. But a move against you also causes delta to deteriorate faster.

Theta — Time Decay as a Percentage

Theta = Change in Option Price / Change in Time (1 day)

While far OTM options appear to decay less in absolute rupee terms, they decay much faster as a percentage of their premium. A Rs. 35 far OTM option losing Rs. 1.50/day is losing ~4.3% of its value daily, versus an ATM at Rs. 300 losing Rs. 8/day (~2.7%).

Payoff Scenarios: Rupee-by-Rupee Comparison

The table below shows the same directional trade idea executed at three different strikes. The underlying is Nifty at 21,000 with 30 days to expire. All values are per lot (50 units).

| Scenario | ATM (21,000 CE) | OTM (21,500 CE) | Far OTM (22,000 CE) |

|---|---|---|---|

| Nifty spot at trade entry | 21,000 | 21,000 | 21,000 |

| Strike selected | 21,000 CE (ATM) | 21,500 CE (OTM) | 22,000 CE (Far OTM) |

| Premium paid | Rs. 300 | Rs. 120 | Rs. 35 |

| Delta | ~0.50 | ~0.25 | ~0.10 |

| Breakeven at expiry | 21,300 | 21,620 | 22,035 |

| P&L if Nifty at 21,300 | +Rs. 0 (breakeven) | -Rs. 120 (full loss) | -Rs. 35 (full loss) |

| P&L if Nifty at 21,500 | +Rs. 200 | -Rs. 120 (full loss) | -Rs. 35 (full loss) |

| P&L if Nifty at 22,000 | +Rs. 700 | +Rs. 380 | -Rs. 35 (full loss) |

| P&L if Nifty at 22,500 | +Rs. 1,200 | +Rs. 880 | +Rs. 465 |

| Required move to profit | +1.4% (300 pts) | +3.0% (620 pts) | +4.9% (1,035 pts) |

Reading the table: Illustrative payoff example based on stated assumptions. Notice that far OTM requires a 4.9% rally just to break even, while ATM only needs 1.4%. Far OTM options typically require larger underlying price movements before they acquire significant value.

Expected Value Framework

Expected Value = (Probability of Profit x Avg Gain) – (Probability of Loss x Premium Paid)

🔹 ATM Option: P(profit) ~45%, Avg gain moderate — EV is often close to zero or slightly negative (by design of options pricing)

🔹 Far OTM Option: P(profit) ~5–10%, Avg gain large in rare scenarios — EV is deeply negative in most market conditions

Options are fairly priced by market makers. Far OTM options are not mispriced for bargains — the low premium correctly reflects the low probability. Buying many far OTM contracts does not improve expected value; it just increases variance.

Note: Far OTM options generally have a lower probability of finishing in-the-money, while ATM options tend to be more sensitive to underlying price movement. Actual outcomes depend on market conditions, volatility, time to expiry, and pricing.

Intrinsic Value vs. Time Value — The Component Breakdown

The formula is;

Option Premium = Intrinsic Value + Time Value + Volatility Premium

🔹 Intrinsic Value: ATM = Rs. 0. Far OTM = Rs. 0. Neither has intrinsic value unless deep ITM.

🔹 Time Value: Higher for ATM options because there is a ~50% chance they end up ITM. Far OTM has lower time value.

🔹 Volatility Premium (Vega component): ATM options carry the highest vega — they gain the most when implied volatility (IV) rises. Before a major event (Union Budget, RBI Policy), ATM options are generally more sensitive to changes in implied volatility than far OTM options.

When to Use Which Strike — Scenario-Based Guide

Neither ATM nor far OTM is universally superior. The right choice depends on your specific trade setup, time horizon, and risk tolerance.

| Trading Scenario | Commonly Used Strike Type | Reasoning |

|---|---|---|

| Short-term directional trade (1–5 days) | ATM | High delta = faster reaction to move |

| Event-based trade (earnings, budget) | ATM or slight OTM | Captures vol expansion without too much theta risk |

| Low-cost speculative lottery | Far OTM | Max loss = premium; requires large move |

| Hedging a long portfolio | Slight OTM Put | Cheaper than ATM; acceptable protection level |

| Selling premium (as writer) | ATM / slight OTM | Highest time decay collected as writer |

| Bull/Bear spread (defined risk) | ATM buy + OTM sell | Reduces cost by selling far OTM against ATM |

| High IV environment (expected to fall) | ATM (sell) | Captures vol crush; not far OTM (low premium) |

Note: The examples, probabilities, and payoff illustrations in this article are hypothetical and provided solely for educational purposes. They should not be interpreted as recommendations, forecasts, or indications of future performance.

Conclusion

The debate around ATM vs Far OTM Options is about choosing a trade with better behavior, not just cheaper entry. While far OTM options may allow more quantity, they often bring lower probability and faster time decay risk.

An at the money option is usually closer to the current price, more responsive, and easier to align with a trader’s view. Understanding the characteristics of different strike prices may help traders evaluate option exposures more effectively.

Do You Find This Interesting?

We’d Love to Hear from you-

Frequently Asked Questions

What is at the money option?

An option whose strike price equals or is very close to the current market price. It has little/no intrinsic value but a maximum time value.

What is out of the money?

An option with no intrinsic value: a call whose strike is above market price, or a put whose strike is below it.

What does delta mean for ATM vs OTM?

ATM delta is ~0.50 (moves Rs. 0.50 per Rs. 1 move in underlying). Far OTM delta is ~0.05–0.15 (barely reacts to small moves).

Are far OTM options ever the right choice?

Far OTM options are sometimes used for speculative positioning, hedging structures, or multi-leg strategies. Suitability depends on individual objectives, risk tolerance, and market conditions.

What is the breakeven for an ATM call?

Strike + Premium paid. For a 21,000 CE bought at Rs. 300, breakeven = Rs. 21,300 at expiry.

DISCLAIMER: Investment in securities market are subject to market risks, read all the related documents carefully before investing. The securities quoted are exemplary and are not recommendatory. Full disclaimer: https://bit.ly/naviadisclaimer.