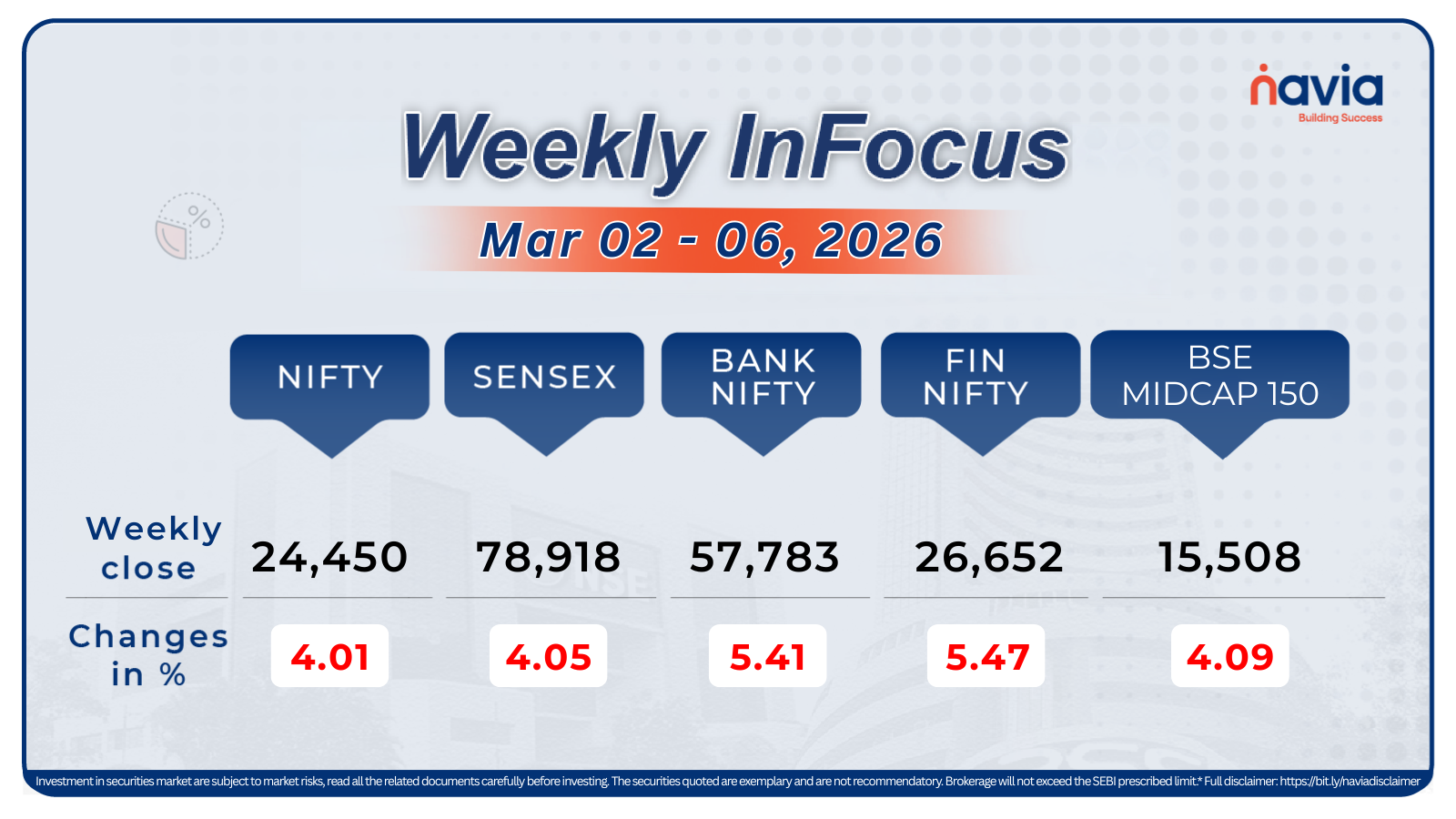

Navia Weekly Roundup (Mar 02 – 06, 2026)

- Week in the Review

- Indices Analysis

- Interactive Zone!

- Sector Spotlight

- Top Gainers and Losers

- Currency Chronicles

- Commodity Corner

- Top Blogs of the Week!

- N Coins Rewards

Week in the Review

In the truncated week, Indian equity markets remained under pressure amid escalating geopolitical tensions between the US and Iran, which led to a sharp jump in crude oil prices. Weak global cues, a declining rupee, and persistent FII selling further weighed on investor sentiment.

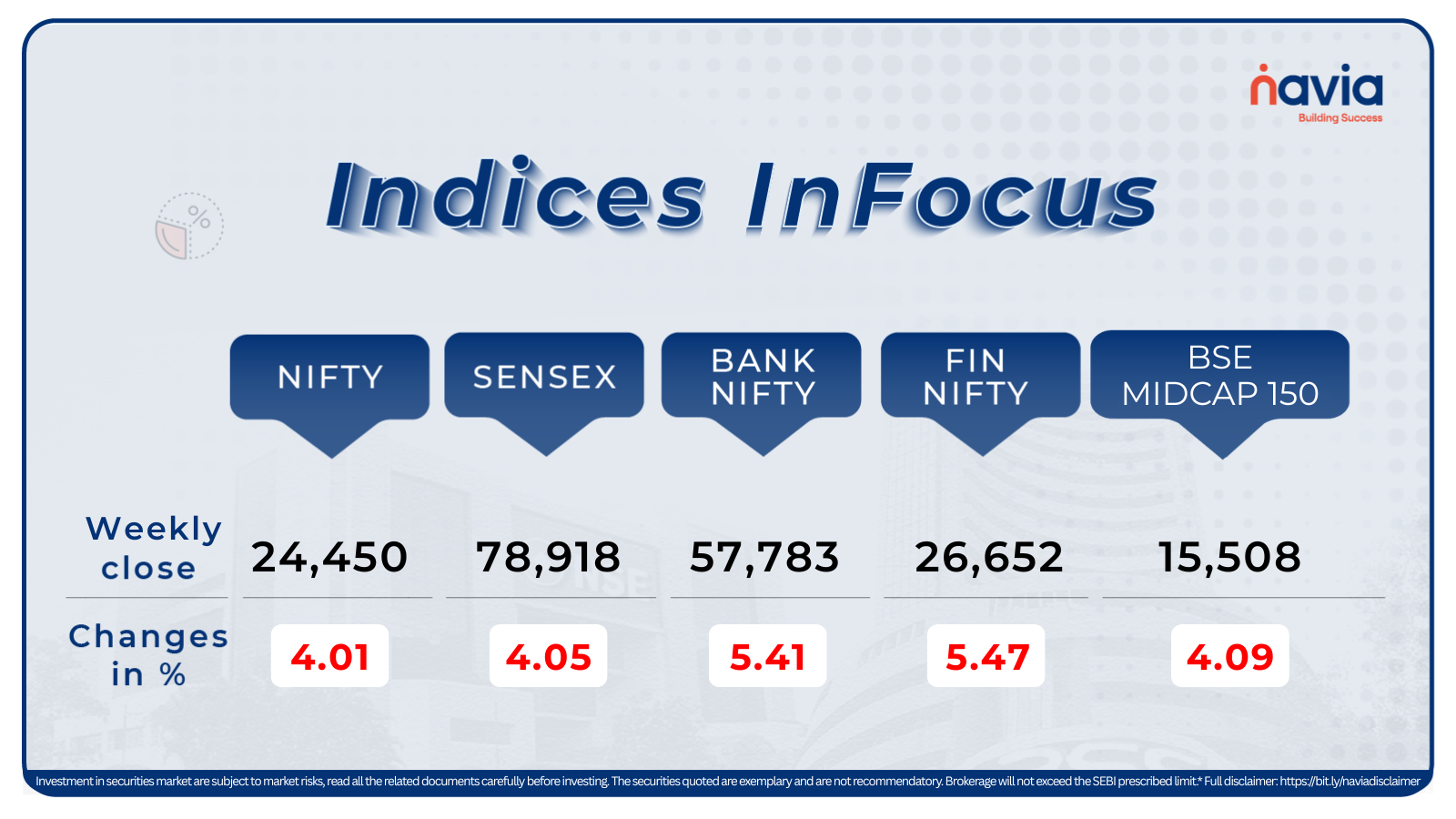

Indices Analysis

During the week, the BSE Sensex slipped 4.05 percent, to finish at 78,918.90, while the Nifty50 shed 4.01 percent, to close at 24,450.45.

The BSE Smallcap index fell 3.3 percent during the week, with InfoBeans Technologies, Worth Investment & Trading, Orchid Pharma, Sadhana Nitrochem, Rajesh Exports, Netweb Technologies India, Agarwal Industrial Corporation, JTL Industries, D. P. Abhushan, Stallion India Fluorochemicals falling between 15-25 percent. On the other hand, Jindal Poly Films, Jindal Drilling Industries, Hindustan Oil Exploration Company, Ruby Mills, Paras Defence and Space Technologies, Antelopus Selan Energy, Axtel Industries, Sterlite Technologies, and Jupiter Wagons added between 12 and 25 percent.

The BSE Largecap index fell 3 percent during the week, with Indian Oil Corporation, Lodha Developers, Adani Green Energy, Interglobe Aviation, Bharat Petroleum Corporation, Tata Motors Passenger Vehicles, Bosch, GAIL India, Godrej Consumer Products, Bank Of Baroda fell between 8-10 percent, while gainers were Solar Industries India, Mazagon Dock Shipbuilders, Bharat Electronics, Hindalco Industries, Sun Pharmaceutical Industries.

The BSE Midcap index shed 3 percent during the week, dragged by Aegis Vopak Terminals, Petronet LNG, Rail Vikas Nigam, LT Technology Services, KPIT Technologies, Bank of India, while gainers included National Aluminium Company, United Breweries, Bharat Dynamics, JSW Infrastructure.

Interactive Zone!

Test your knowledge with our Markets Quiz! React to the options and see how your answer stacks up against others. Ready to take a guess?

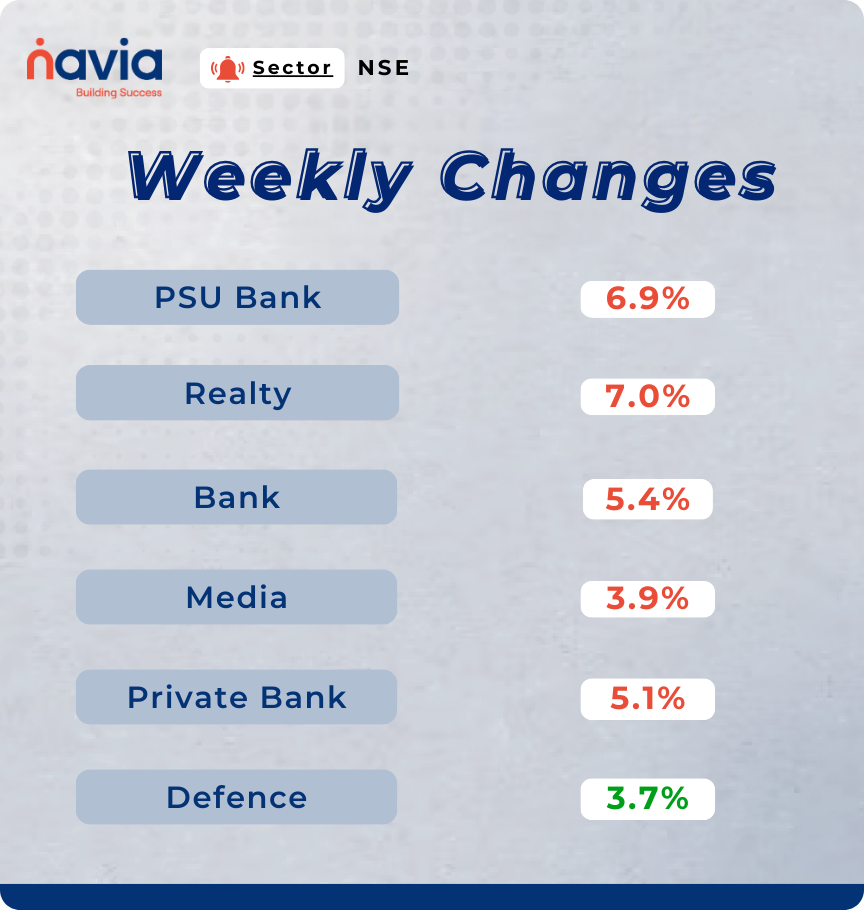

Sector Spotlight

Most sectoral indices ended in the red during the week. The Nifty PSU Bank index declined 6.9 percent, followed by the Nifty Realty index, which fell 7 percent. The Nifty Bank index dropped 5.4 percent, while the Nifty Media index slipped 3.9 percent and the Nifty Private Bank index shed 5.1 percent. However, the Nifty Defence index bucked the trend, gaining nearly 3.7 percent.

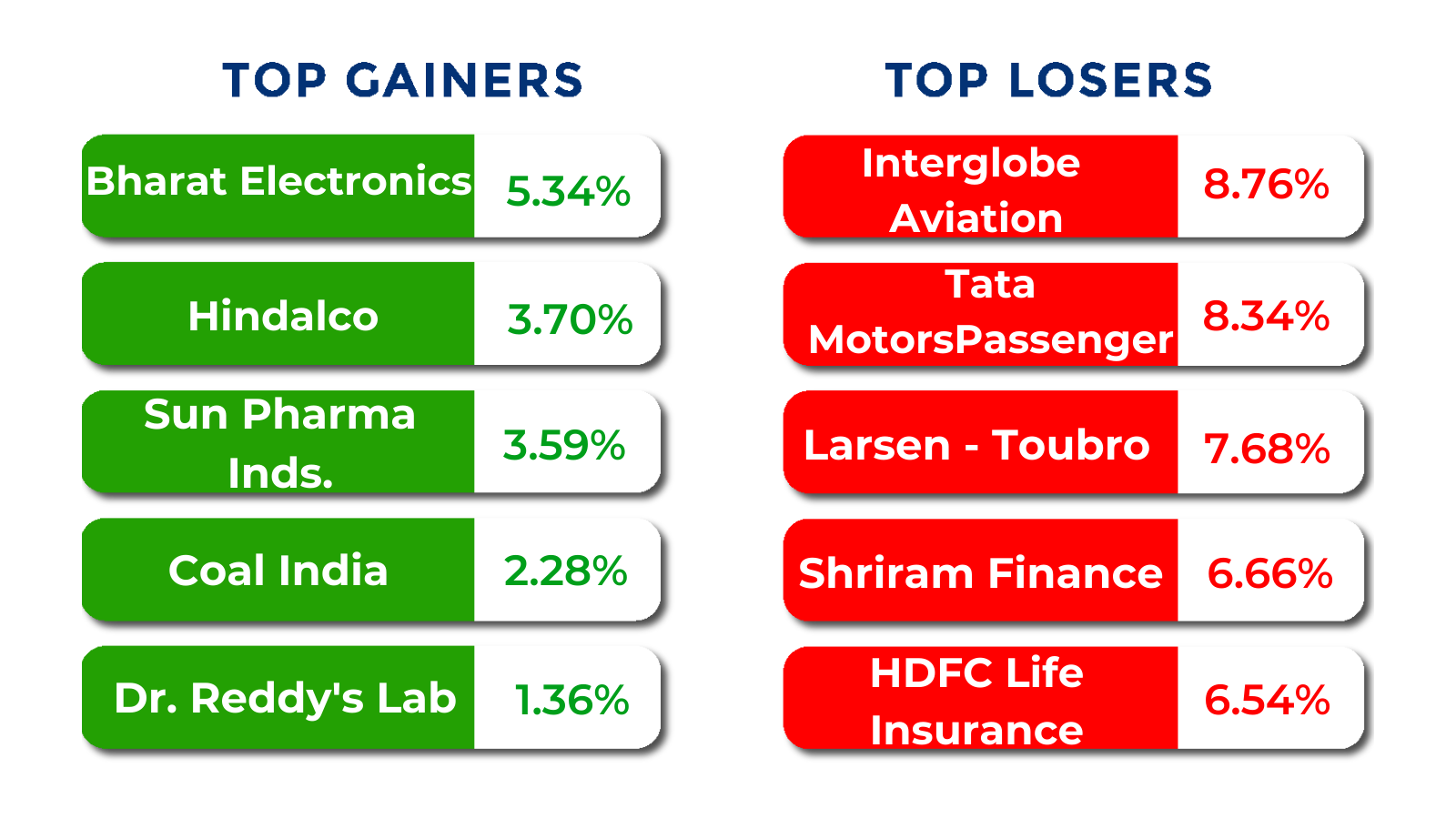

Top Gainers and Losers

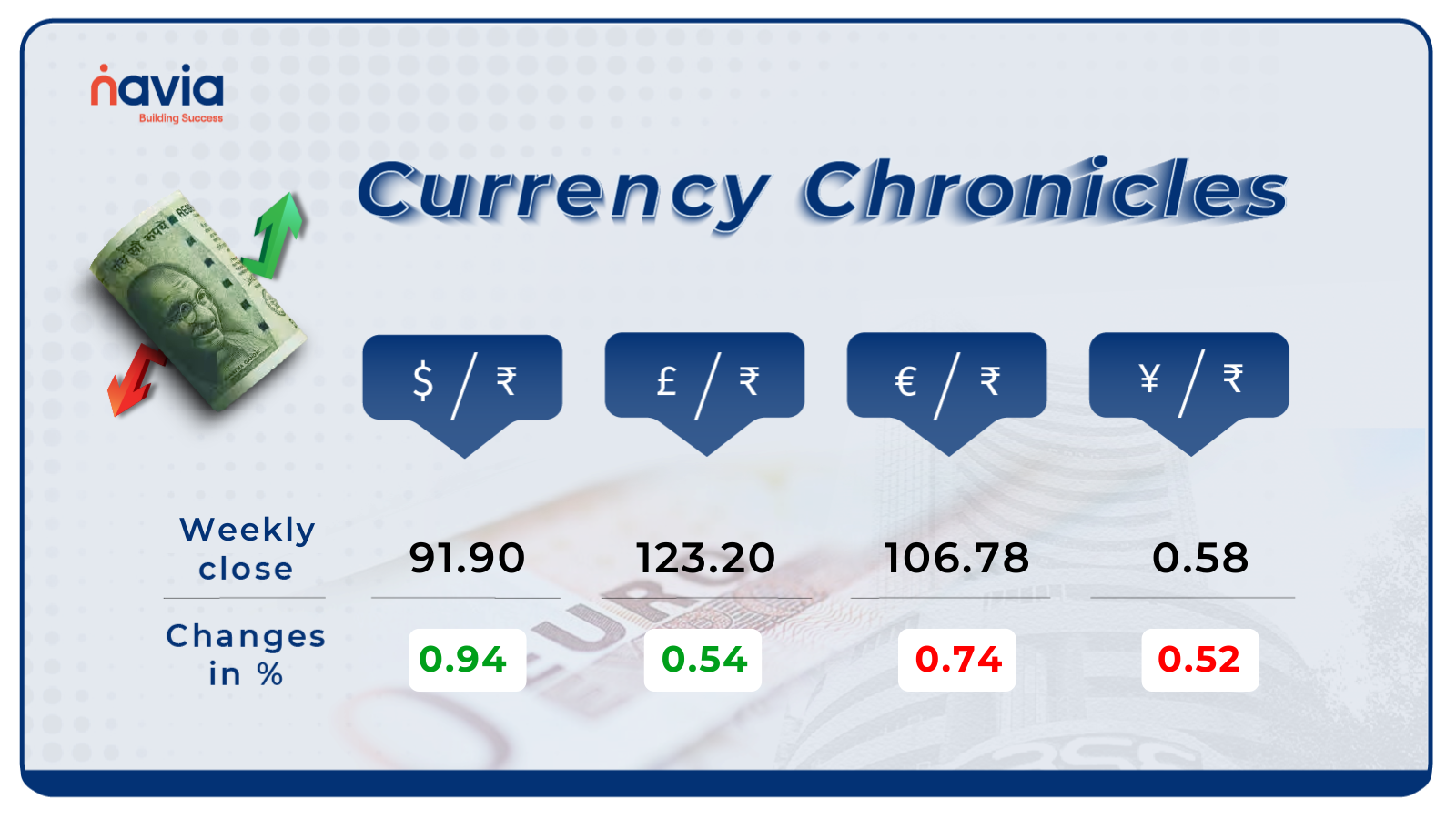

Currency Chronicles

USD/INR:

The USD/INR rate closed at ₹91.90 per dollar, gaining 0.94% during the week, reflecting a bullish market sentiment.

EUR/INR:

The EUR/INR rate closed at ₹106.78 per euro, losing 0.74% during the week, reflecting a bearish market sentiment.

JPY/INR:

The JPY/INR rate closed at ₹0.58 per yen, losing 0.52% during the week, reflecting a bearish market sentiment.

Stay tuned for more currency insights next week!

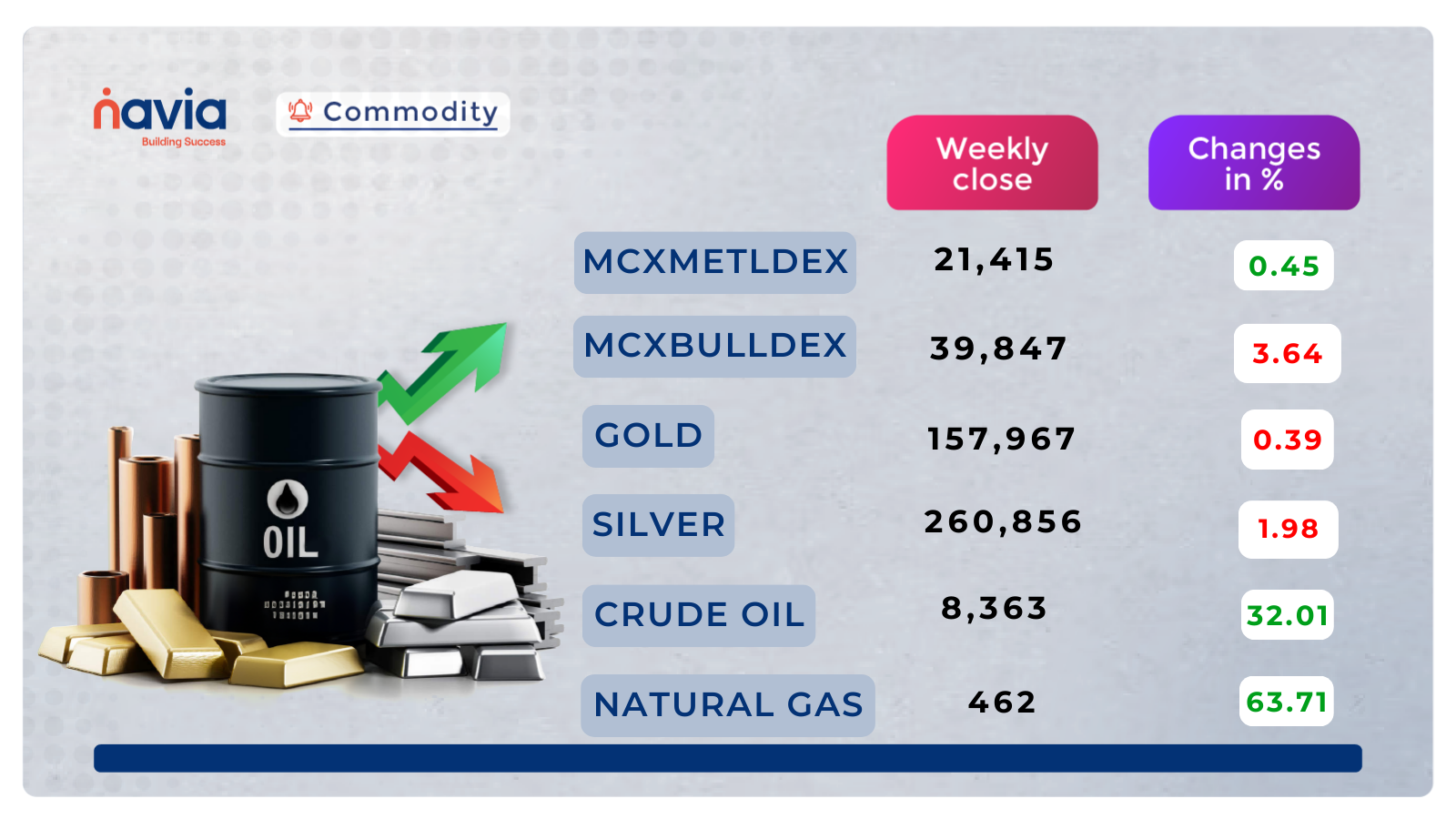

Commodity Corner

Crude Oil futures are currently trading near 7353, extending the strong bullish momentum after the decisive breakout above the previous resistance zone at 6126–7000. The price has formed an impulsive series of higher highs and higher lows, with the latest green candle closing near session highs, confirming continued buying pressure and acceleration on the higher timeframe. The overall structure is strongly bullish, supported by the ascending trendline from the 5642 base, now well below the current levels. The breakout from the 6800–7000 consolidation area has been followed by sustained follow-through, pushing price toward the 7340–7400 extension zone. Short-term consolidation or minor pullback is possible after the sharp rally, but momentum remains firmly in favor of buyers. A sustained move above 7400 could open further upside toward 7600–7800 levels.

Gold futures are currently trading near 159920, consolidating in a tight range just below the immediate resistance zone around 160858–162000. Price continues to hold higher lows from the strong demand base near 150523–152000, preserving a short-term bullish structure supported by the ascending trendline connecting recent swing lows. The current consolidation near 159920–160858 shows small-bodied candles and low volatility, indicating hesitation and balance between buyers and sellers near the upper boundary of the recent advance. The area around 160858 remains a key supply barrier, with multiple prior tests showing rejection. A decisive breakout and sustained close above 160858–162000 could confirm renewed bullish momentum and target 166400–169000 or further toward 172000 levels. On the downside, immediate support lies near 158000–159000, followed by stronger structural support at 150523–152000. A breakdown below 158000 may invite short-term corrective pressure toward 150523–148000 levels.

Natural Gas futures are showing modest recovery strength and consolidating just above the major demand zone around 257.9–260 after the extended downtrend from the January/February peak near 650–600 levels. The price has formed a higher low in recent sessions, with the latest green candle closing near the upper end, indicating short-term buying interest and potential exhaustion of selling pressure near the bottom of the multi-month descending channel. The broader structure remains bearish overall, guided by the descending trendline from the February highs, which continues to act as dynamic resistance and has capped upside attempts. However, repeated tests of the 257.9–260 support cluster have held, creating a possible base for short-term reversal if momentum builds. A decisive breakdown and sustained close below 257.9 could accelerate downside toward 230–220 levels. On the upside, immediate resistance lies near 297.7–300, followed by stronger supply at 320–350 and the descending trendline. A sustained breakout and close above 300 would signal short-term bullish reversal potential and open relief rally toward 350–410 levels.

Silver futures are currently trading near 262200, consolidating in the mid-to-upper part of the recovery range after a steady climb from the February lows. Price has maintained a clear higher low structure off the major demand base near 231368–257971, with the ascending trendline from late February lows continuing to provide dynamic support and guiding the short-term bullish bias. The broader structure remains range-bound between the strong demand zone at 231000–240000 and the persistent supply/resistance area around 280000–291941. The current zone near 260000–263500 is acting as short-term support during minor pullbacks, while repeated tests of the 262000–265000 area show buyer absorption. A decisive breakout and sustained close above 292000 could trigger fresh bullish momentum toward 305000 and further to 333000–333278 levels. On the downside, immediate support lies at 257971–260000, followed by stronger demand near 250000 and the major zone at 231368. A breakdown below 257971 may invite short-term profit booking or renewed weakness toward 245000–231000.

Do you have a question? Ask here and we’ll publish the information in the coming weeks.

Top Blogs of the Week!

Understanding Pharmabees ETF: An Overview of Healthcare Sector Exposure

The Nippon India Nifty Pharma ETF (PHARMABEES) remains a cornerstone for investors looking to gain diversified exposure to India’s pharmaceutical powerhouse. As of March 2026, the sector continues to show resilience, serving as a “defensive” play amidst global market shifts.

Beyond Support and Resistance: How to Accurately Identify Supply and Demand Zones

In the 2026 trading environment, relying solely on thin horizontal support and resistance lines can be like trying to catch a waterfall with a straw. To trade with precision, you must understand Supply and Demand Zones.

N Coins Rewards

Refer your Friends & Family and GET 500 N Coins.

Do You Find This Interesting?

DISCLAIMER: Investment in securities market are subject to market risks, read all the related documents carefully before investing. The securities quoted are exemplary and are not recommendatory. Full disclaimer: https://bit.ly/naviadisclaimer.